For most of DeFi’s history, the dominant architectural pattern has been the vertical monolith. A protocol set out to build everything inside its own perimeter. The matching engine, the order book, the lending markets, the staking layer, the yield aggregator, the oracle dependencies, the bridging surface, the front-end. If a product surface existed in the category, the protocol’s roadmap included building it from scratch. The teams that chose this pattern did so not out of architectural preference but out of necessity. The partner infrastructure that would have allowed them to route to someone else’s superior implementation either did not exist or did not work reliably enough to build a serious product against.

That constraint is no longer the constraint. The partner infrastructure has caught up. Perpetual futures engines now expose builder codes that allow a consumer application to route order flow into a production-grade matching layer without re-implementing the engine. Prediction markets are now offered through protocols that have spent years building the oracle stack and the resolution mechanics, and a consumer application can integrate the market surface directly without building either layer. Oracle networks have matured to the point where reliable price feeds are an integration question rather than a research problem. Cross-chain messaging has settled into a smaller number of widely-trusted protocols. Wallet infrastructure has compressed what used to be five engineer-months of work into a single library call.

What this means for the next generation of DeFi applications is structural, not aesthetic. The architectural decision a team faces in 2026 is fundamentally different from the decision a team faced in 2020. The earlier team had to choose between building everything in-house at lower quality or shipping nothing. The current team can choose between building everything in-house at lower quality, or routing the layers that someone else has already built to a higher standard and focusing internal engineering on the layers that are genuinely the team’s edge. The teams that compound fastest are the teams making the second choice consistently.

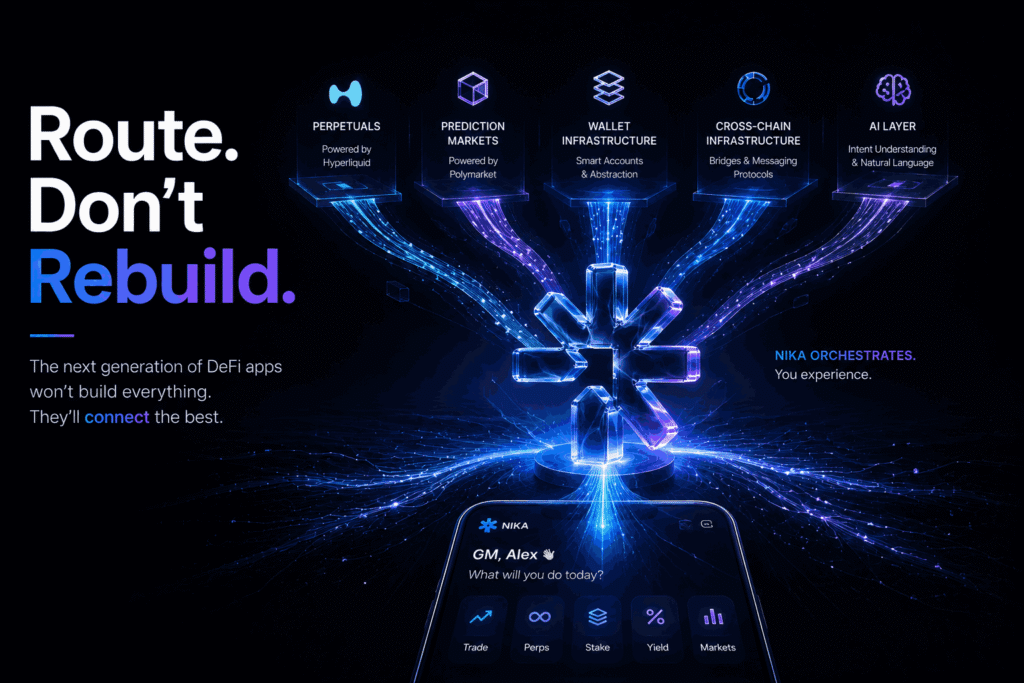

The pattern that has emerged from that choice is the orchestrator application. The orchestrator builds the consumer interface, the wallet, the cross-chain plumbing, the account abstraction, the AI layer, and the connective tissue that makes the full product surface feel unified to the user.Everything else routes.

There are three things this pattern does well that the monolithic model struggles with. The first is shipping cadence. An orchestrator with three or five engineers can ship a new product surface in weeks because the new surface is largely an integration. A monolithic protocol with thirty engineers needs months to build the same surface to a comparable standard because every layer is internal work. The second is quality at the routed layer. The infrastructure protocols the orchestrator is routing to have spent years specializing in their layer. A consumer app that routes to one of them gets a best-in-class implementation as a starting baseline. A monolithic protocol building its own version of that layer is competing with that specialized team using a fraction of the engineering attention. The third is brittleness. When one layer of an integrated application fails or needs revision, the orchestrator can swap the partner without rebuilding the rest of the application. The monolithic protocol has to fix the layer itself, which means downtime and engineering overhead the orchestrator does not carry.

A useful example of the orchestrator pattern in production is Nika Finance, a non-custodial application combining spot trading, perpetuals, staking, yield, and prediction markets powered by Polymarket across multiple chains in a mobile-first interface. The team operating it is three people. The perpetuals layer is powered by Hyperliquid through builder codes, which is a concrete instance of the routing pattern: rather than build a matching engine from scratch, the team routes order flow into the production-grade engine Hyperliquid has spent years building, and focuses internal engineering on the consumer interface, the wallet, the cross-chain plumbing, and the AI layer through which users interact with the full product surface in plain language. The prediction-market surface follows the same logic. The user sees one application. The architecture underneath is a routing graph.

“Most teams are still trying to build everything themselves. The teams moving fastest are the ones integrating the best infrastructure available and focusing their engineering effort on the user experience.” said Daniel Brinzan, founder of Nika Finance.

The teams that resist this pattern are not foolish. They are mostly teams whose roadmaps were locked in an earlier era of DeFi when the routing option did not exist, or teams whose internal political economy makes the build-everything decision easier to defend than the route-everything decision. There is also a category of monolithic projects whose unit economics depend on capturing every layer of the value chain inside their own protocol, which makes routing to a partner unattractive even when the partner’s implementation is better. These teams are not going to disappear, but the gap between their shipping cadence and the orchestrator cohort’s shipping cadence is becoming visible enough that the difference shows up in user growth, retention, and product breadth per engineer.

The implication for the next several years of DeFi is that the architectural decision has consequences that compound. An orchestrator that has been routing well for two cycles will have shipped more product surface, accumulated more user feedback, and iterated more times than a monolithic competitor that started at the same time. The gap is not closeable with additional headcount on the monolithic side. The monolithic team is solving a different problem from the orchestrator. The orchestrator’s edge is not that it is faster at building infrastructure. The orchestrator’s edge is that it has decided not to build most of the infrastructure at all.

What this also means for the partner protocols on the receiving end of the routing is that their distribution surface has multiplied. Hyperliquid does not need to ship a consumer interface to be present in every consumer application that routes to it. Polymarket does not need to win the front-end battle to be the prediction-market engine inside every application that integrates it. The infrastructure protocols and the consumer orchestrators are two halves of the same architectural shift, and the value generated in each half is structural to both sides rather than competitive between them.

Monolithic DeFi was a phase. The phase made sense while the partner infrastructure was being built. The phase is ending. The next generation of consumer-facing DeFi applications is being built around the assumption that the partner infrastructure exists and is reliable, and that the right place to invest internal engineering is in the layers users actually see. That is the architectural decision. The teams that made it early are the teams compounding now. The teams that did not are running out of cycles to adapt before the gap becomes too wide to close.